Basics of Charitable Giving & Tax Planning Strategies

Many taxpayers use charitable giving to reduce their tax liability while supporting the issues they find most important. This article examines some important considerations you need to make when planning and making charitable contributions.

These considerations include various deduction limitations, types of property contributed and various planning strategies you can employ when making charitable contributions.

Limitations & Types of Property Contributed

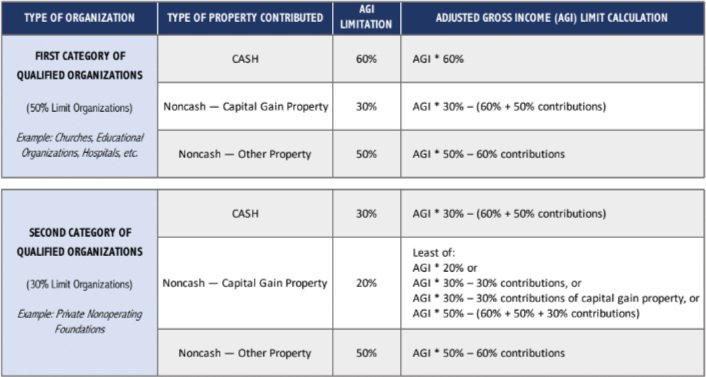

The deduction you can claim for charitable contributions is based on the fair market value (FMV) of the property contributed, the type of property donated and the charity receiving the donation. For example, the deduction claimed for a cash donation is different than the deduction claimed for a contribution of stock. The table to the right summarizes the various limitations and the order for claiming a charitable deduction.

Tax Planning Strategies

Following the passing of the Tax Cuts and Jobs Act of 2017, far fewer taxpayers claim itemized deductions on their tax returns. This could result in a charitable contribution providing no tax benefit since a taxpayer must itemize their deductions to claim a charitable contribution deduction for federal tax purposes.

We will look at different tax planning strategies related to charitable giving that still allow a taxpayer to receive the tax benefit of their charitable giving.

APPRECIATED ASSETS

One strategy is to donate appreciated assets. Because the deduction for donated property held for more than a year is generally based on the FMV of the property donated, taxpayers should consider donating property that is worth substantially more than the original purchase price or basis. These assets could include stocks, real estate or any other appreciated assets.

By donating the property instead of selling the asset and donating the cash, the taxpayer can avoid paying tax on any gains from the sale and receive a charitable contribution deduction. Further, the charitable organization will not have to recognize income and pay tax on the eventual sale of the asset.

However, if the donated property is not cash or publicly traded securities and the value of the contributed property is $5,000 or more, the taxpayer must have the property appraised by a qualified appraiser. Further, the qualified appraisal must be attached to the return if the deduction claimed is $500,000 or more. Failure to provide a qualified appraisal in the year of the contribution will result in a disallowance of the deduction.

BUNCHING

Another common strategy is called “bunching.” Bunching is when the taxpayer saves funds for multiple years and then donates all the funds in one given year when the total contribution is more than the standard deduction. This method is common among taxpayers who do not have substantial itemized deductions outside their charitable contributions. For example, a taxpayer who gives $10,000 per year but has no other itemized deductions would likely claim the higher standard deduction of $27,700 for 2023.

However, if the taxpayer decides to set aside $10,000 per year for five years, the taxpayer could make a charitable contribution of $50,000 in the fifth year and claim the contribution as an itemized deduction when the total itemized deductions are greater than the standard deduction.

DONOR-ADVISED FUND

Taxpayers wishing to supply even contributions of assets to charity could set up a donor-advised fund (DAF) and contribute the $50,000 to the DAF. A DAF is a separate fund managed by a 501(c)(3) organization called a sponsoring organization.

The taxpayer receives a deduction when the funds are contributed to the DAF. The taxpayer can then advise the fund when to make distributions to the charities of their choice.

QUALIFIED CHARITABLE DISTRIBUTION

One other common strategy for charitable giving is called a qualified charitable distribution (QCD). A QCD is a distribution taken directly from your taxable individual retirement account (IRA) and given to a charitable organization without passing through the hands of the IRA owner.

Individuals aged 70.5 and older can contribute up to $100,000 per year to one or more charities. Married couples can contribute up to $200,000 per year by each contributing $100,000. A QCD is a great strategy to implement one or more of the following:

•Satisfy annual required minimum distributions (RMDs).

•Reduce RMDs in future years by reducing the balance of the IRA.

•A QCD excludes the amount donated from taxable income, possibly preventing donors from being pushed into higher-income tax brackets.

Note: A qualified charitable distribution is not included as an itemized deduction for charitable contributions. Essentially, taxpayers are moving the deduction from Schedule A to “above the line,” which can be beneficial if a taxpayer has certain deductions/credits that now may not phase out due to AGI limitations.

•To make a larger charitable gift that doesn’t require AGI limits to apply.

An important reminder to note when choosing to make a QCD is to confirm the receiving organization is qualified to accept QCDs. Starting in 2023, as part of recently passed SECURE Act 2.0 legislation that expanded the type of charities that can receive a QCD, donors can make a one-time gift up to $50,000 to a charitable gift annuity, charitable remainder annuity trust or a charitable remainder unitrust. Also, the QCD annual limit will now be indexed for inflation, starting in 2024.

REQUIRED MINIMUMDISTRIBUTIONS (RMDS)

Employer-sponsored retirement plans, SEP or SIMPLE IRAs and traditional IRAs require an annual amount of money to be withdrawn called an RMD. The Securing a Strong Retirement Act of 2022 (SECURE 2.0 Act) implemented several changes for RMDs and several of these changes are detailed below.

•In 2023, the required RMD beginning date was extended to participants who turn 73 and in 2033, the age limit increases to 75.

•In 2023, a special needs trust that was established for a disabled beneficiary and funded with an inherited IRA is now allowed to retain stretch RMDs over the lifetime of the chronically ill or disabled beneficiary.

•In 2024, the pre-death RMD requirement for Roth 401(k) accounts is eliminated. This was already the case for Roth IRAs and now aligns Roth designated accounts in employer plans.

•In 2024, surviving spouses can elect to be treated as the plan participant for RMD purposes. This allows the surviving spouse to defer the distribution period to begin no earlier than the date of which the deceased spouse would have attained the age of RMDs (73 or 75 as mentioned above). By utilizing this election, the distribution period is determined using the longer uniform lifetime table rather than the single life table.

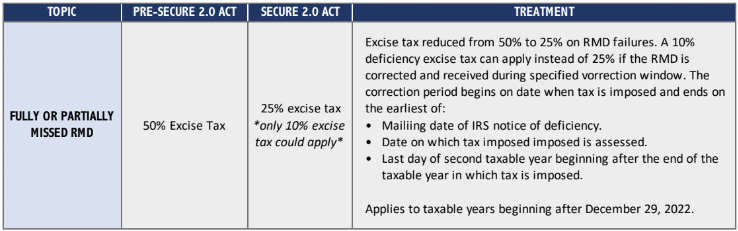

The table below summarizes changes to excise tax.

If you have any questions regarding these tax considerations or need assistance, please contact a tax professional.